AGEAS X OPEN GI CAR INSURANCE —

AGEAS X OPEN GI CAR INSURANCE —

Ageas x Open GI Car Insurance

Re-establish Urban Jungle in the motor insurance market without sacrificing the customer experience that made it successful in home

Overview

Urban Jungle had previously offered car insurance before exiting the market when Wakam, its underwriter, pulled back from motor offerings and stopped investing in new ventures. The relaunch, built on OpenGI with Ageas as the new insurer partner, was the opportunity to come back on Urban Jungle's own terms, with full control over the customer experience and a clear path to scale across PCW, direct, white-label, and cross-sell channels.

I was the sole designer on the project, working closely with engineering and data engineering throughout due to the complexity of the OpenGI third-party software integration.

The Challenge

Motor insurance is one of the most constrained design environments in financial services. Pricing and eligibility are controlled externally via OpenGI APIs, introducing dependencies across UX, data, and operations that don't exist in Urban Jungle's home product.

The challenge was threefold:

Design a fast, low-friction experience within a system where key variables were outside our control

Integrate simultaneously with four third-party platforms: OpenGI, Ageas, Premium Credit, and RAC

Launch a fully functional PCW product in eight weeks as a team of one designer

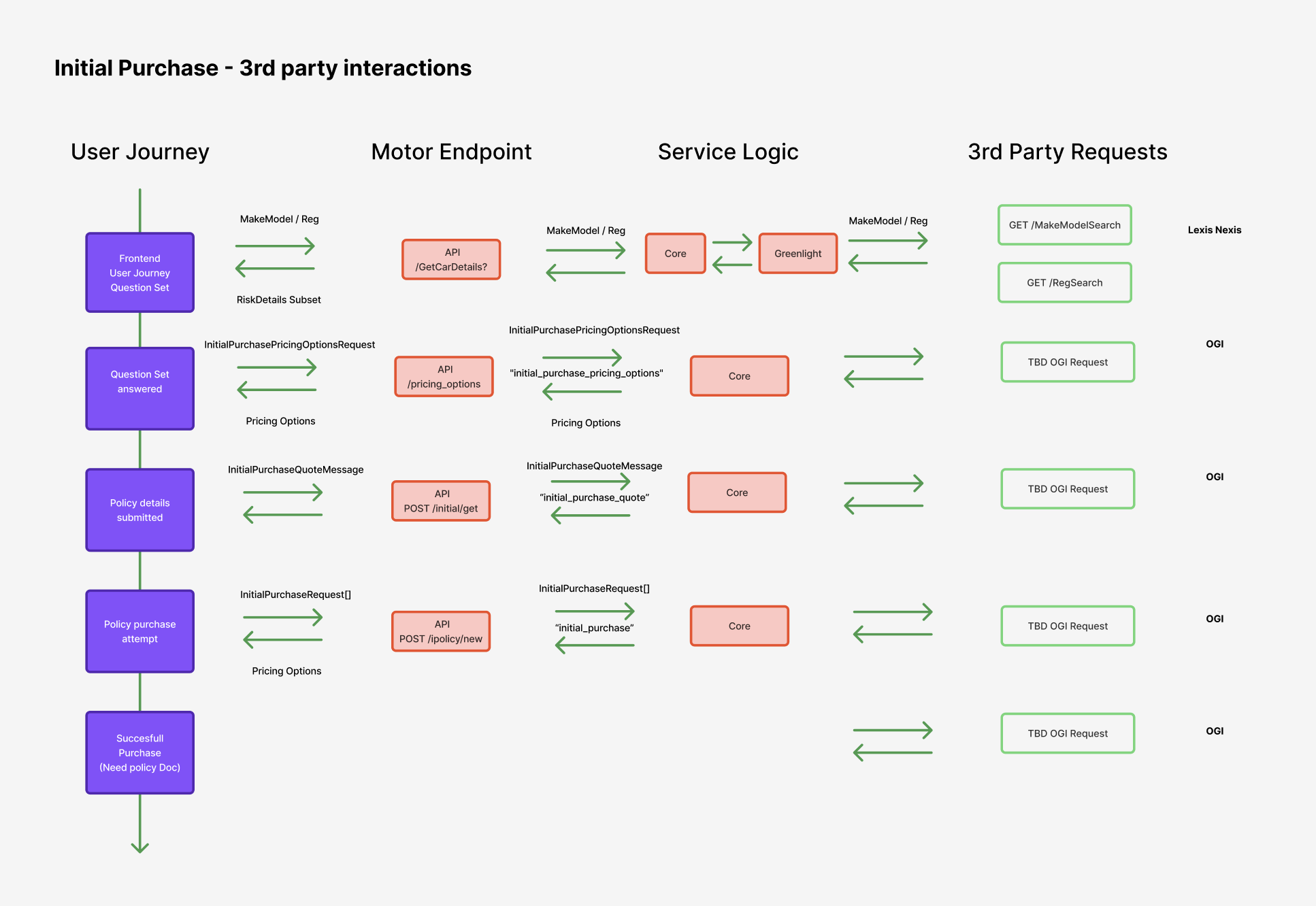

Mapping third-party interactions in order to understand design and build requirements

My Role

Sole designer end-to-end across both phases of the build with full ownership of:

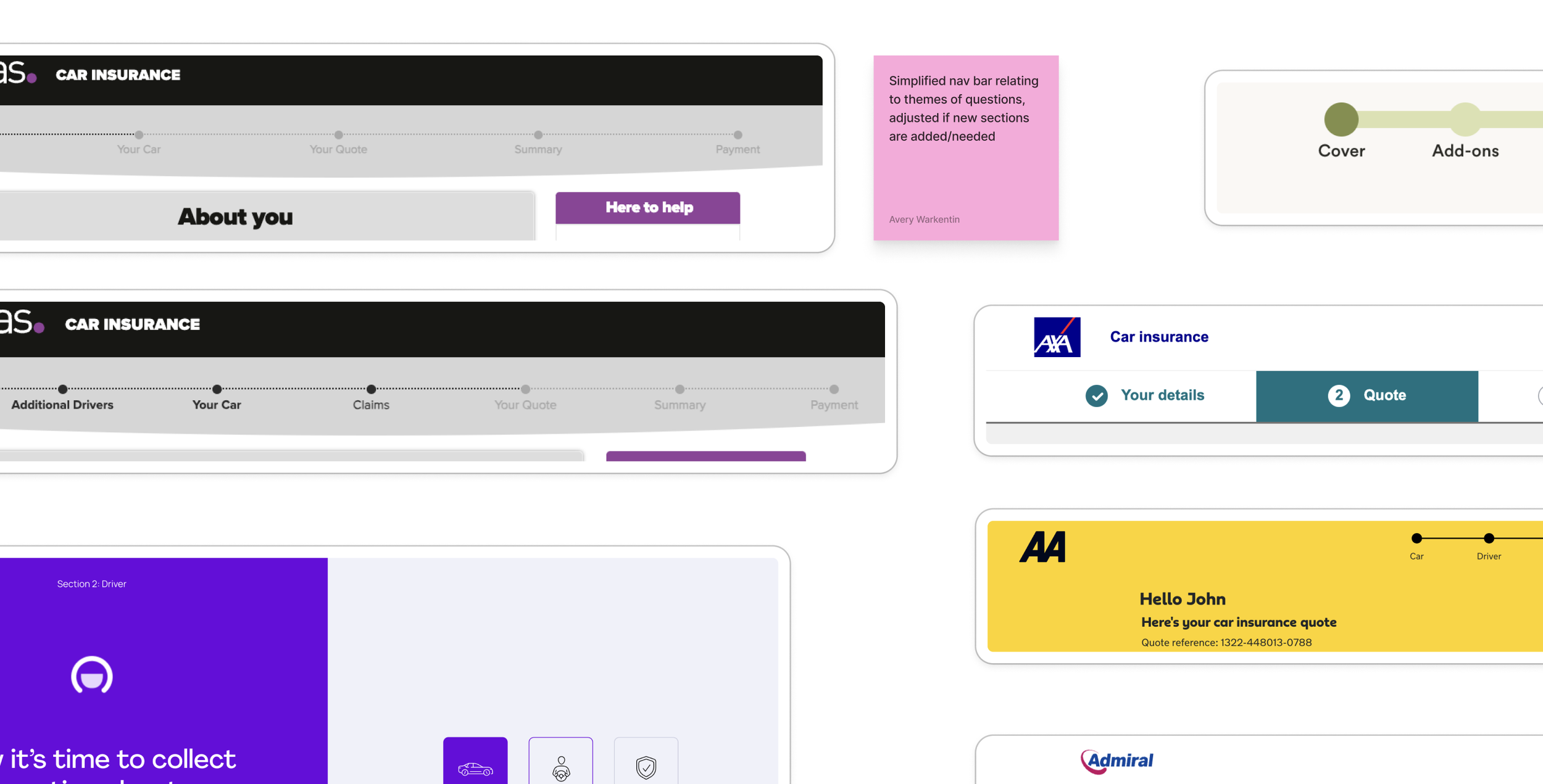

Competitor research and user research via surveys

End-to-end wireframing and prototyping across the full purchase journey and account management

Design sign-off and engineering feasibility with OpenGI, Ageas, Premium Credit, and RAC

Cross-functional collaboration across product, engineering, and commercial teams on PCW integrations

Stakeholder management across multiple external partners simultaneously, with extensive feedback cycles throughout

Mapping the flow of information to understand user journey flow requirements

Timeline

Phase 1 — 8 weeks

Full PCW purchase journey and account management, live at launch

Phase 2 — 6 weeks

Premium finance via Premium Credit, and breakdown and legal add-ons via RAC

After understanding third-party integration requirements, I kicked off the PCW design scoping process with competitor research

Why PCW First?

Price comparison websites dominate UK motor insurance for new business. Over 63% of consumers used a PCW to switch providers in 2024, with Compare the Market alone holding close to 50% of the aggregator market. For a product re-entering a competitive category without an established motor brand presence, PCW was the only viable acquisition channel at launch and the right place to prove the product before investing in direct.

Design Principles

SIMPLICITY

Reduce perceived complexity in a high-friction category

CLARITY

Plain language, minimal jargon, strong information hierarchy

CONSISTENCY

Align with existing UJ journeys to reduce learning curve

MOBILE-FIRST

Optimise for PCW-driven mobile traffic

SCALABILITY

Design patterns that support future insurers and journeys

Design Deep Dive

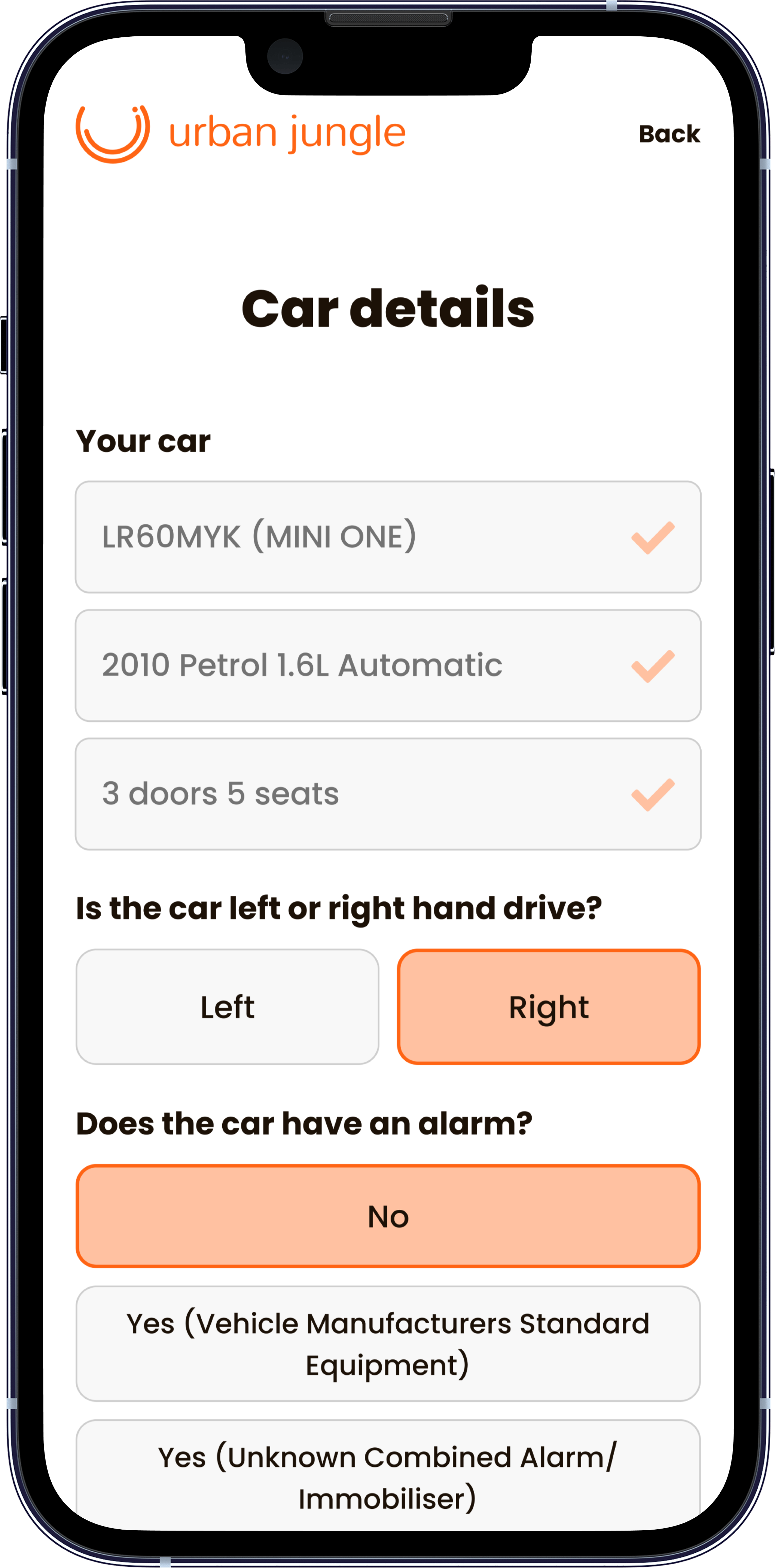

Feature 1: PCW Purchase Journey — Reducing Cognitive Load in a High-Friction Category

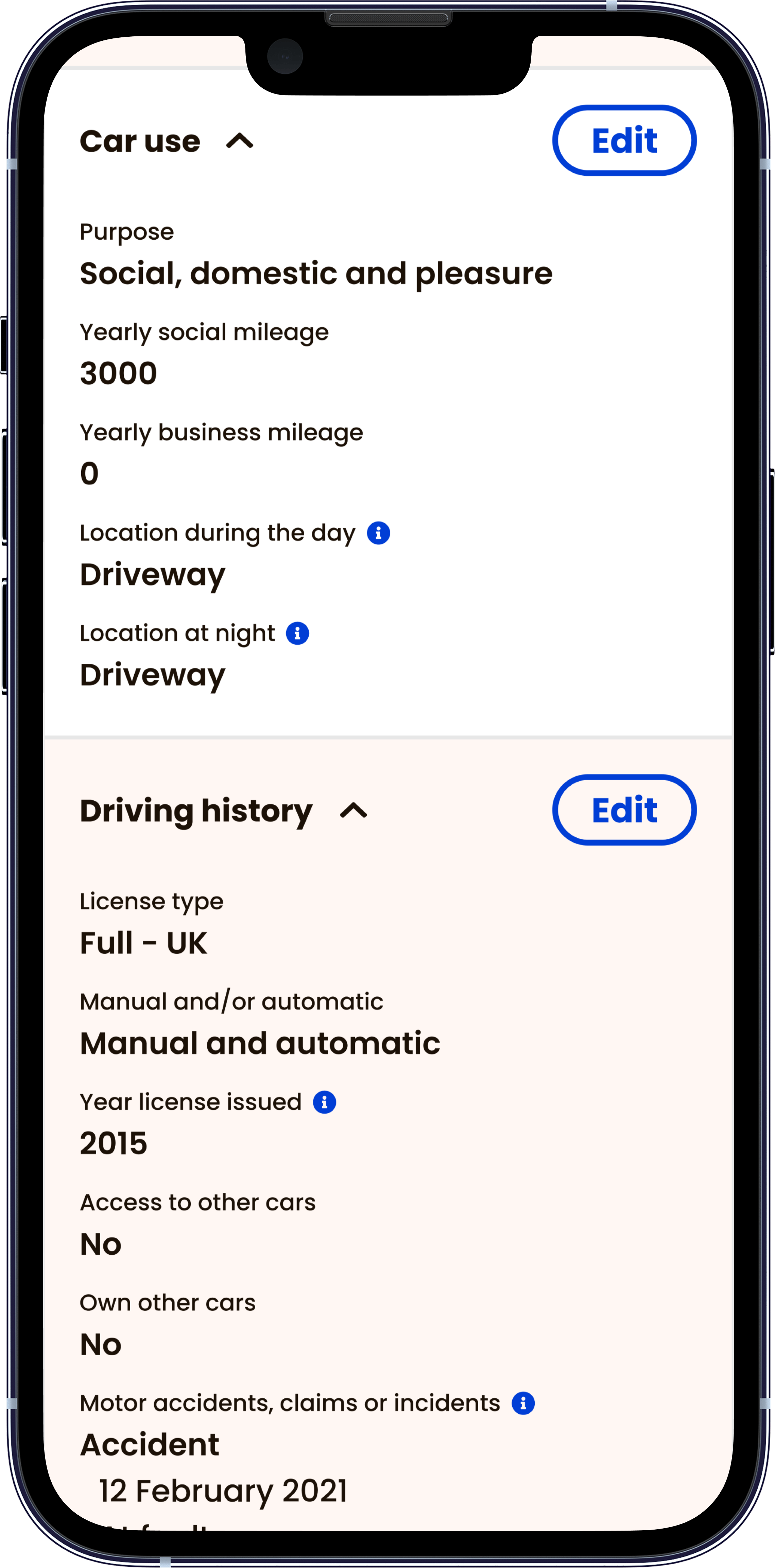

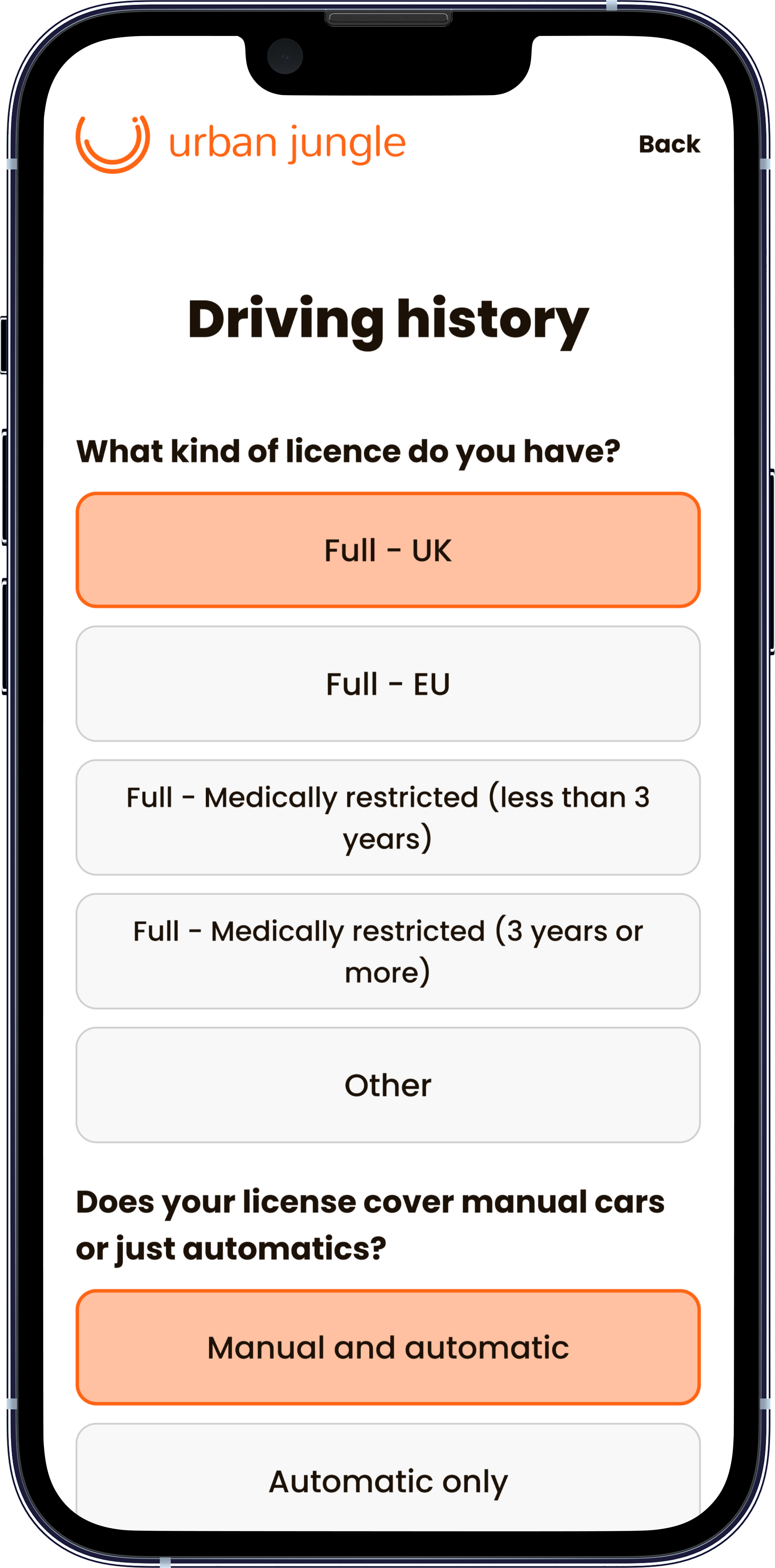

Motor requires significantly more information from customers than home. This includes more questions, stricter eligibility, and more complex data dependencies. The design principles were straightforward: ask only what's required, pre-fill wherever possible, and maintain consistency with existing UJ home journeys to reduce the learning curve for returning customers.

The most technically demanding part was question mapping – translating PCW language into the format OpenGI accepts internally. I contributed to these decisions editorially as well as technically, recommending simpler, plainer language wherever possible to reduce discontinuity at click-out and lower drop-off caused by unfamiliar phrasing across multiple PCW integrations.

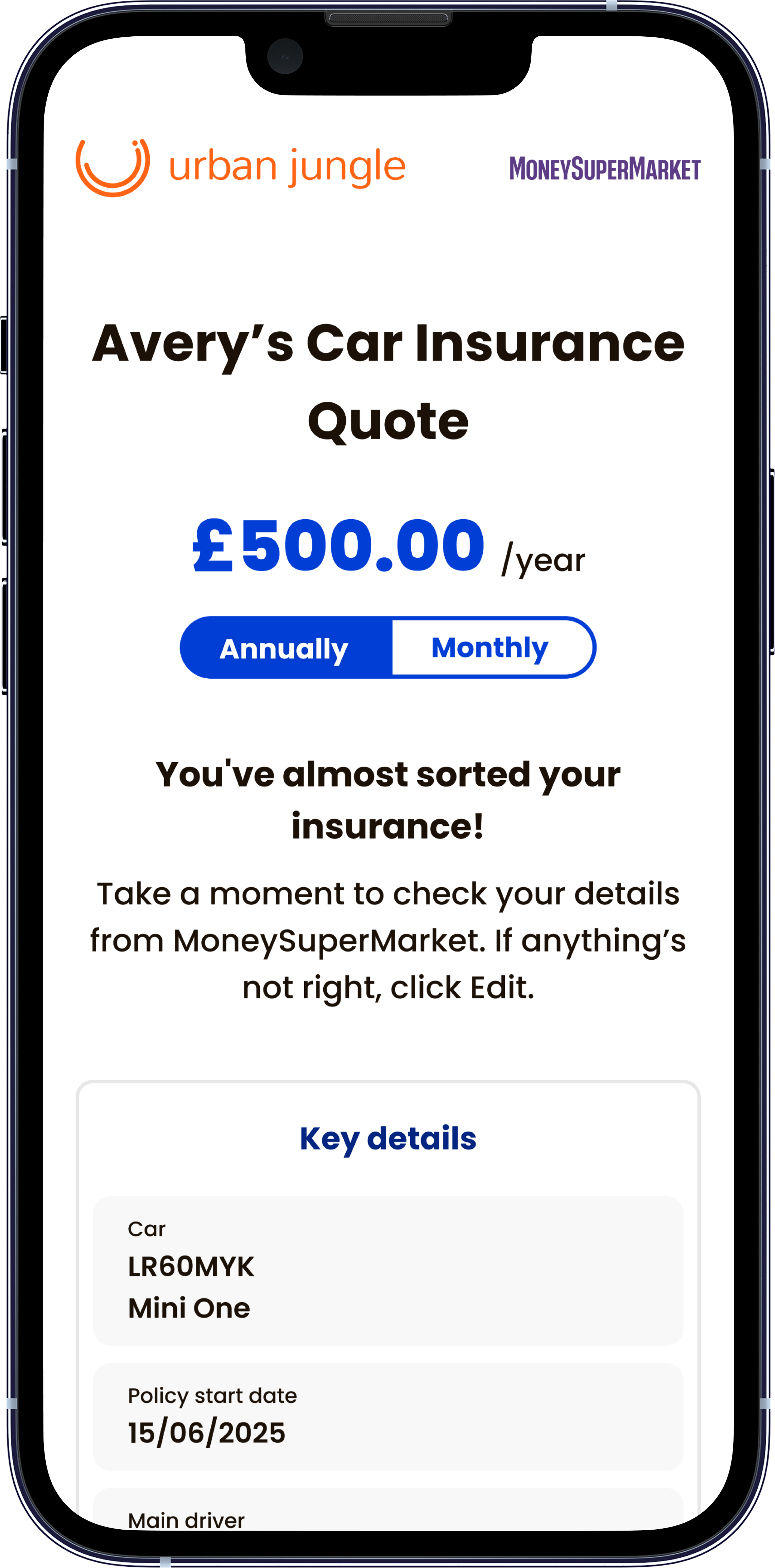

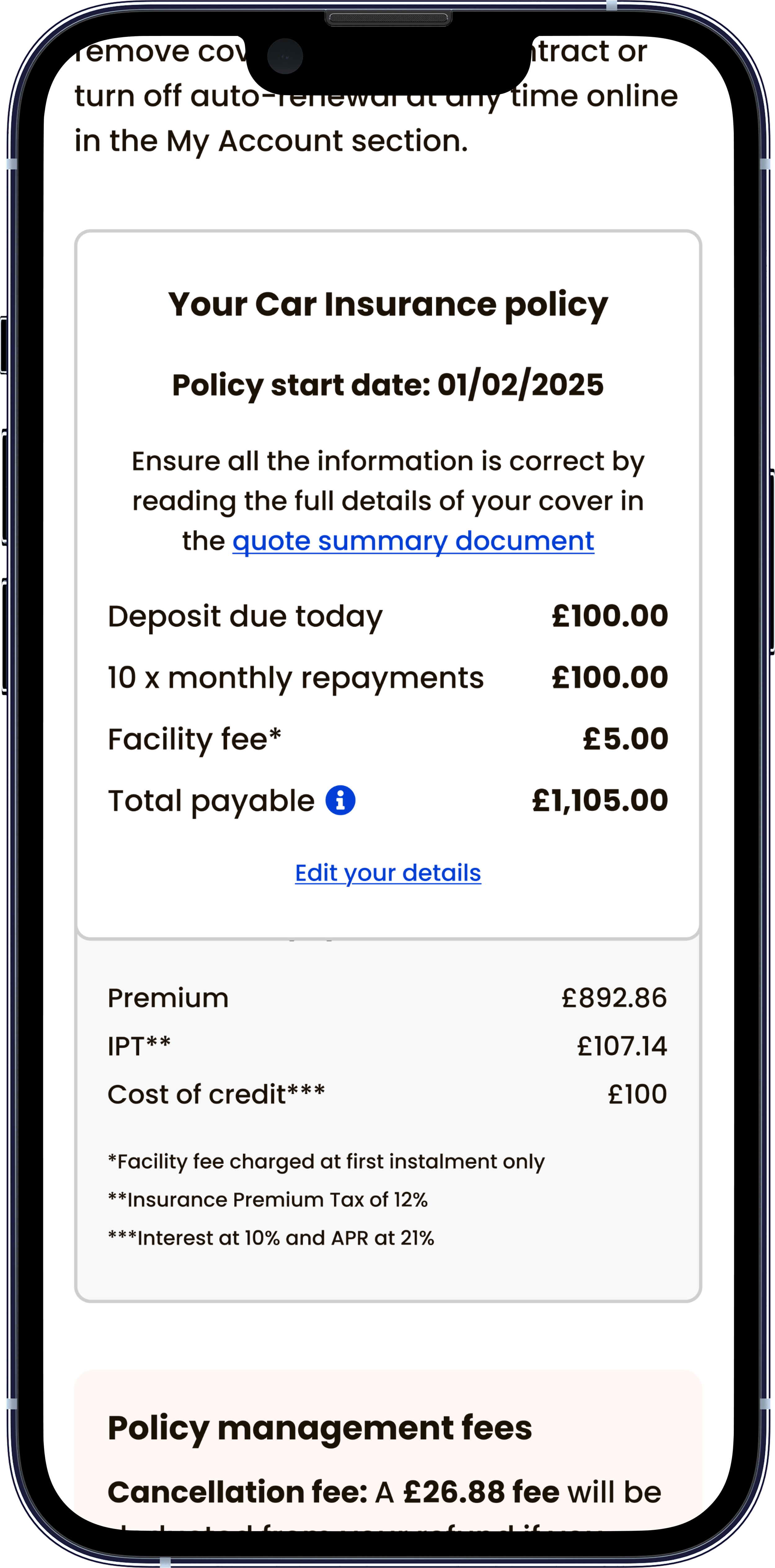

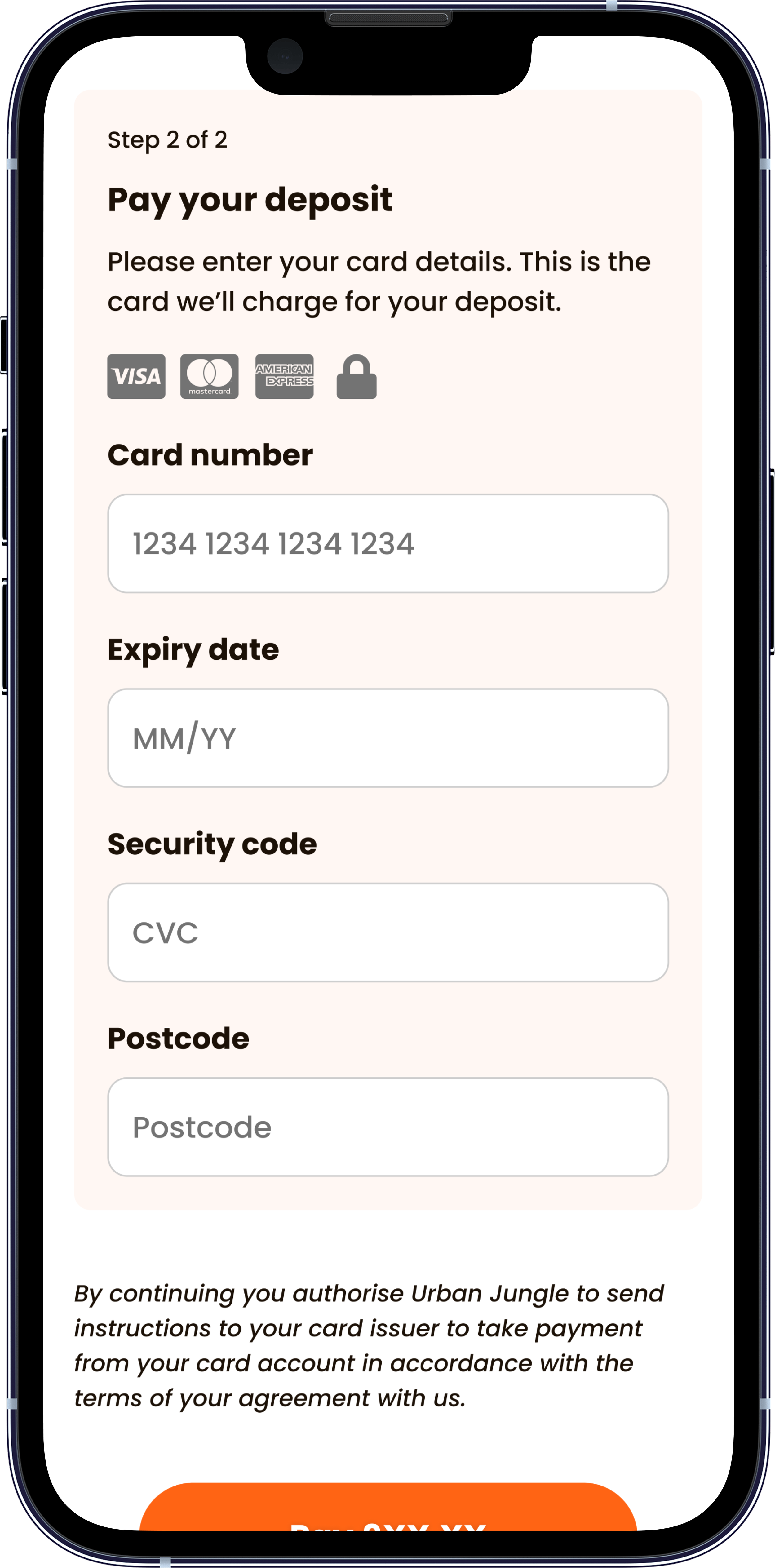

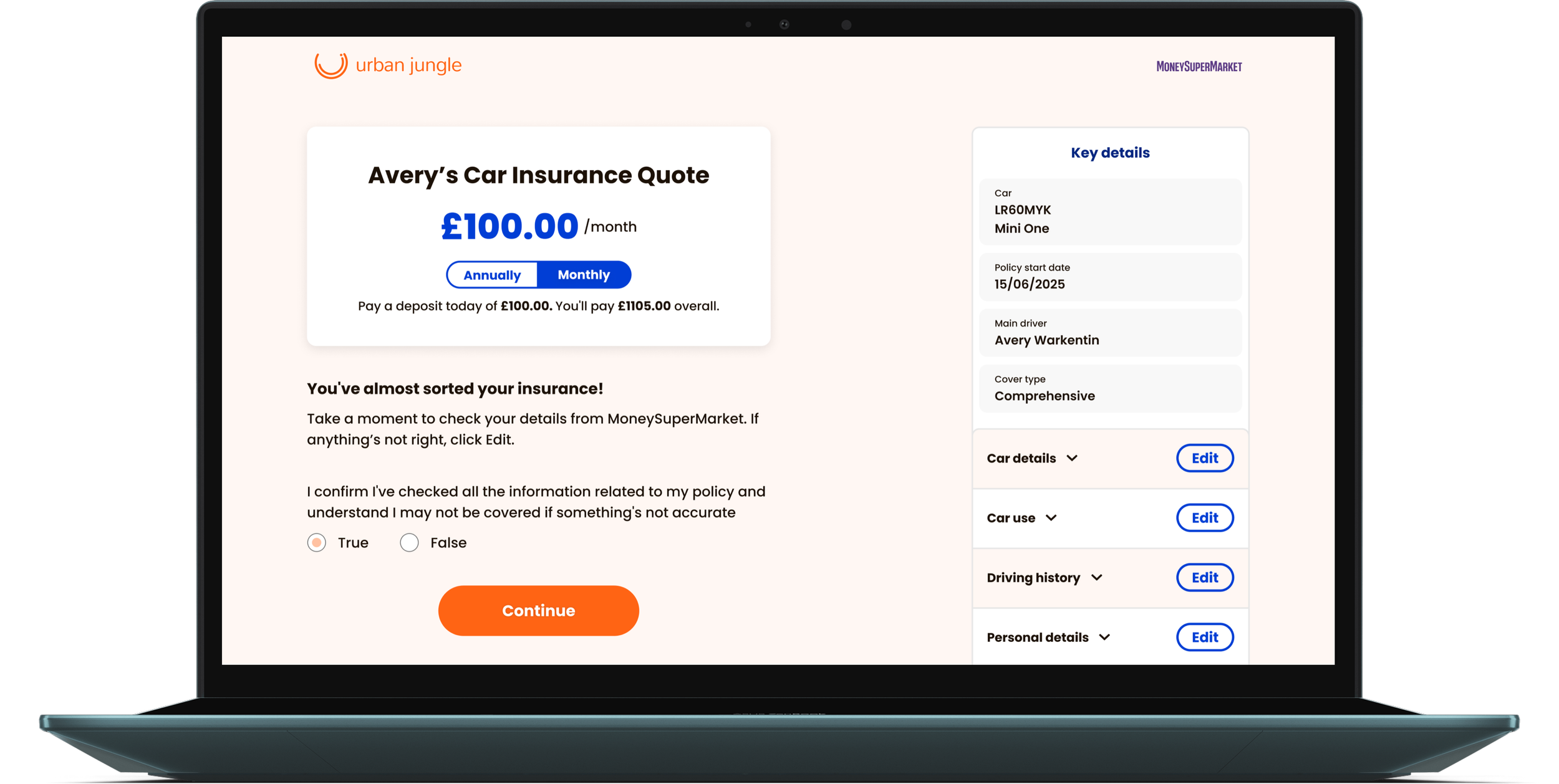

Feature 2: Premium Finance — Making Monthly Payments a First-Class Experience

Around 40% of Urban Jungle's car insurance customers use premium finance to purchase via PCW making payment communication one of the most consequential design decisions in the journey.

The challenge was numerical literacy.

How do you present deposit, monthly payments, IPT, fees, and interest without overwhelming customers mid-journey? The solution was a progressive reveal. We surfaced enough cost information early for customers to make a confident decision, then providing a full breakdown only at the payment page when conversion intent is higher. Showing everything upfront created confusion; hiding it created distrust.

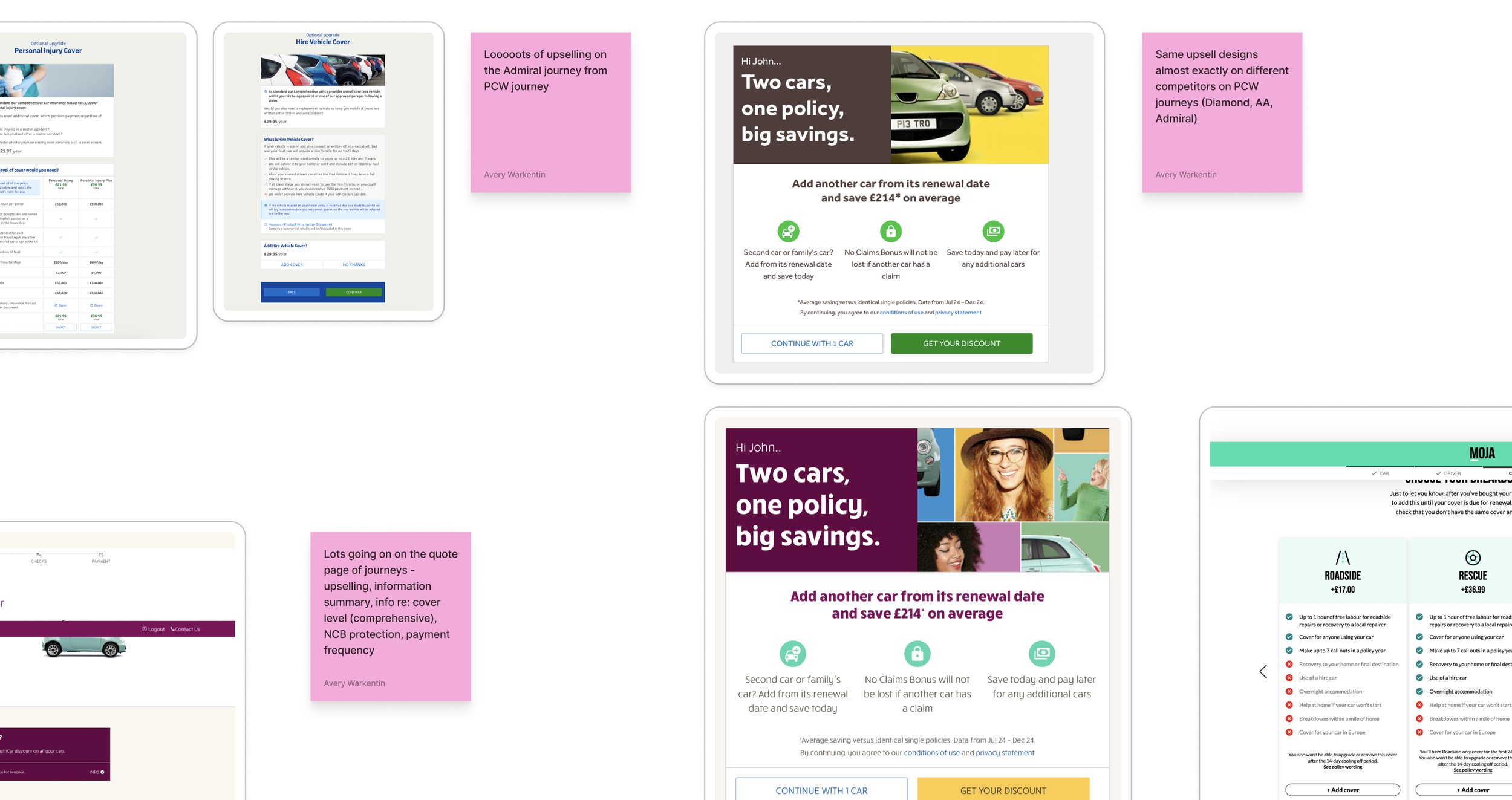

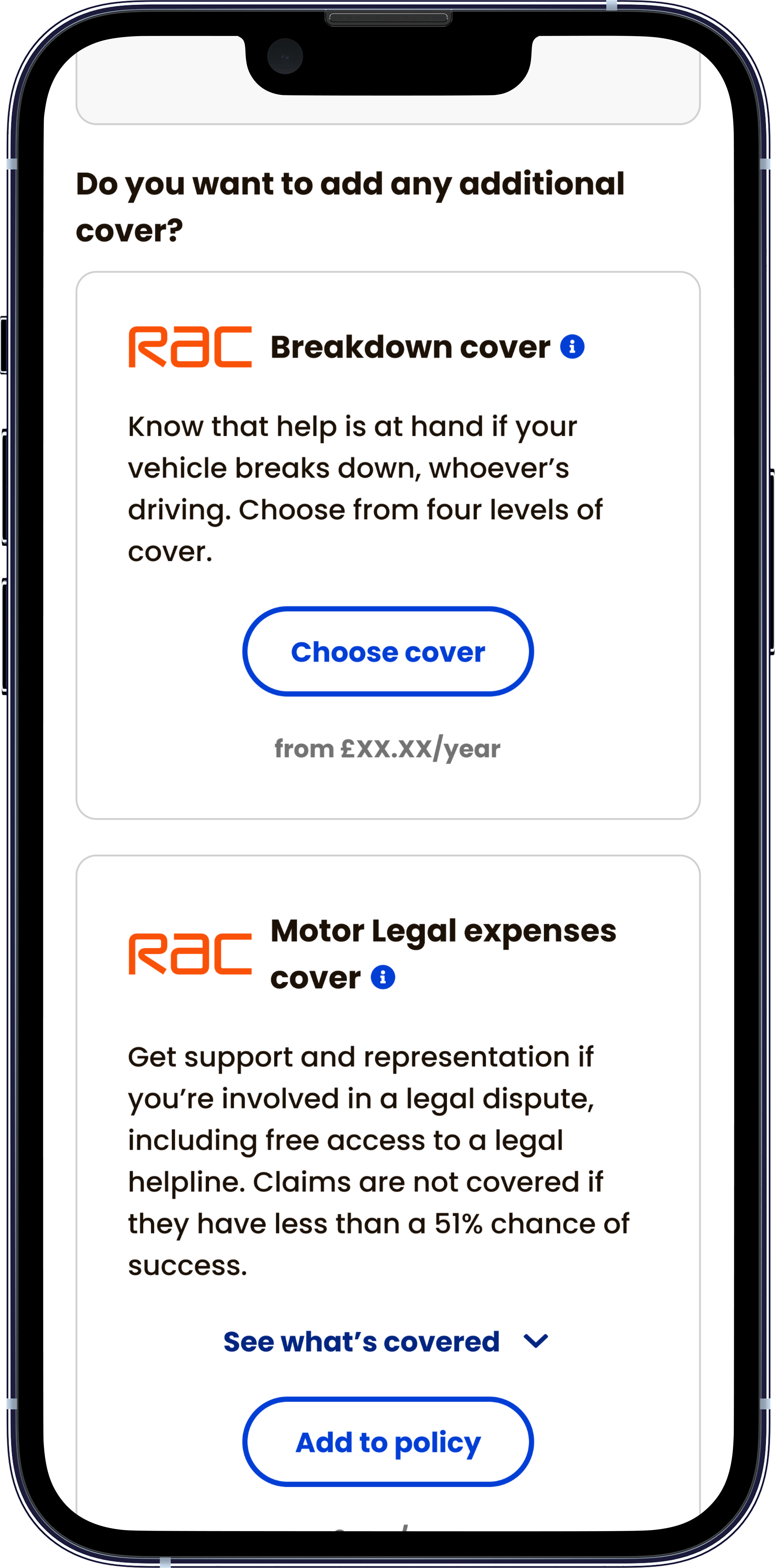

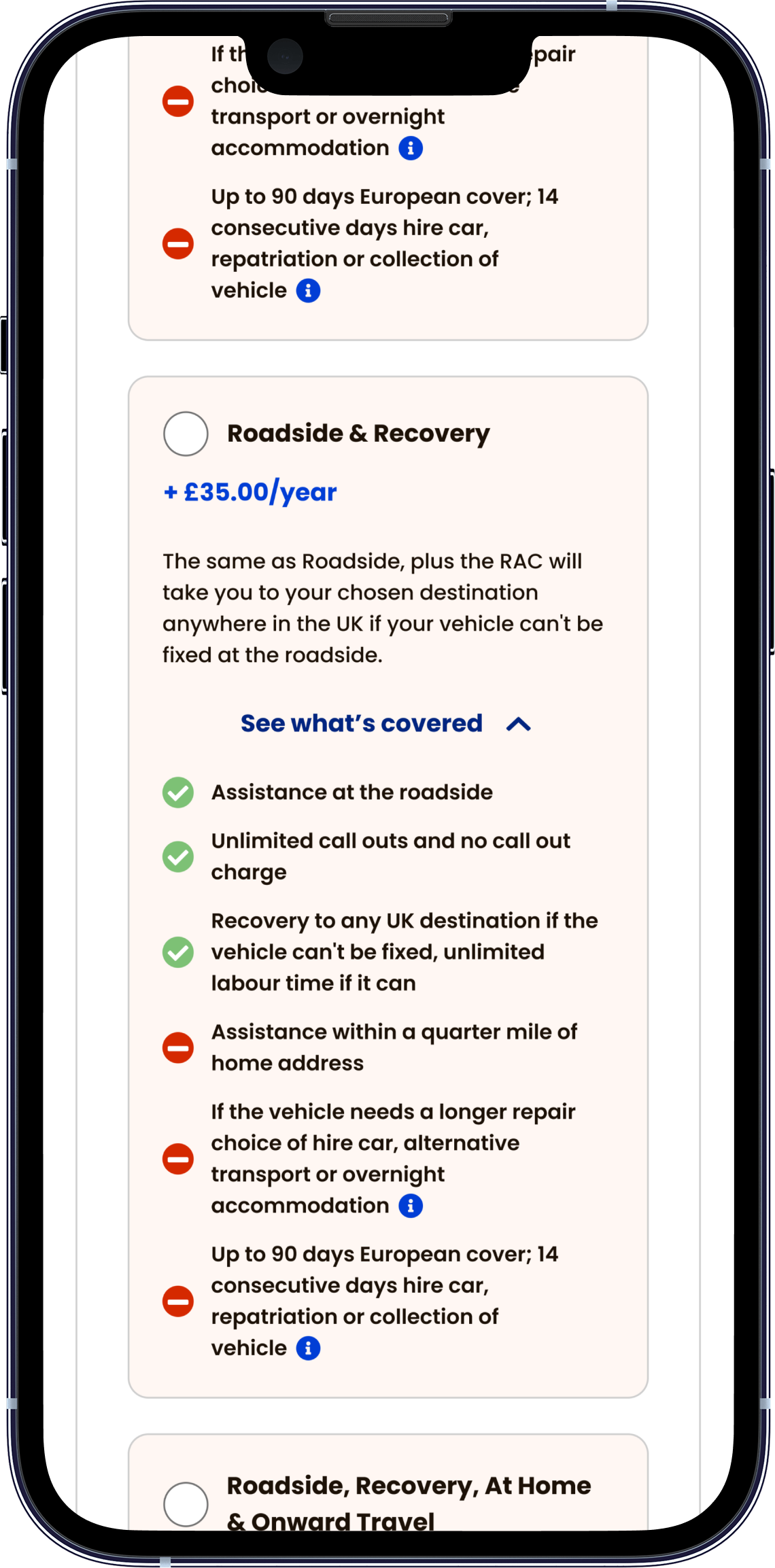

Feature 3: RAC Add-ons — Education Over Upsell

Breakdown and legal cover were introduced via RAC across multiple tiers, with the design focused on helping customers make informed decisions rather than defaulting to upsell. Add-ons were presented as dedicated journey steps to reduce visual conflict with the core flow.

Knowing RAC's sign-off process would take time, I proactively provided branding options early in the relationship to keep approvals moving in parallel with build. Since launch, breakdown cover has seen a 32% uptake rate, with 24% of those customers actively upselling to a higher tier.

I decided to user progressive reveal to reduce the multi-step checkout process for premium finance customers

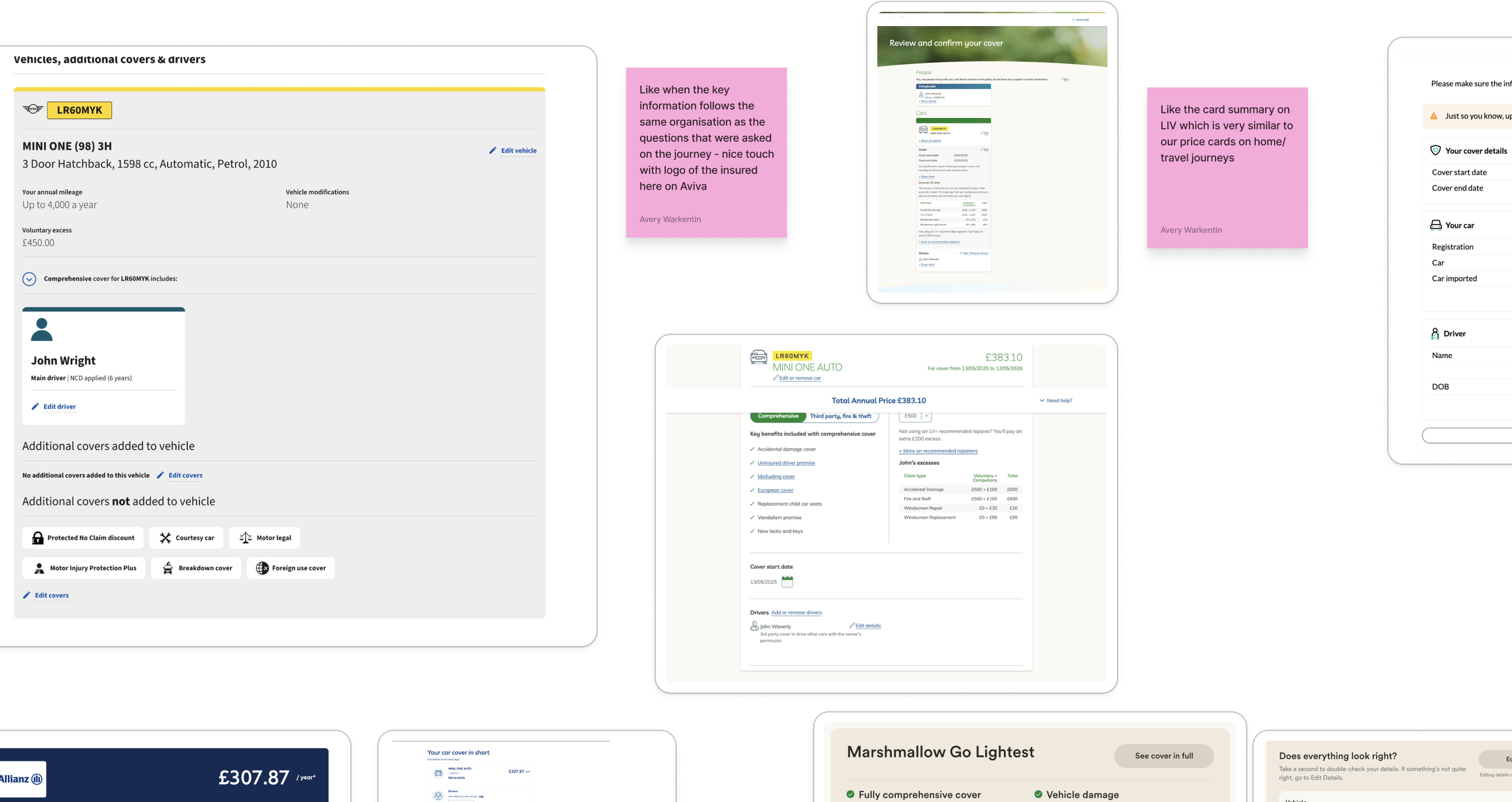

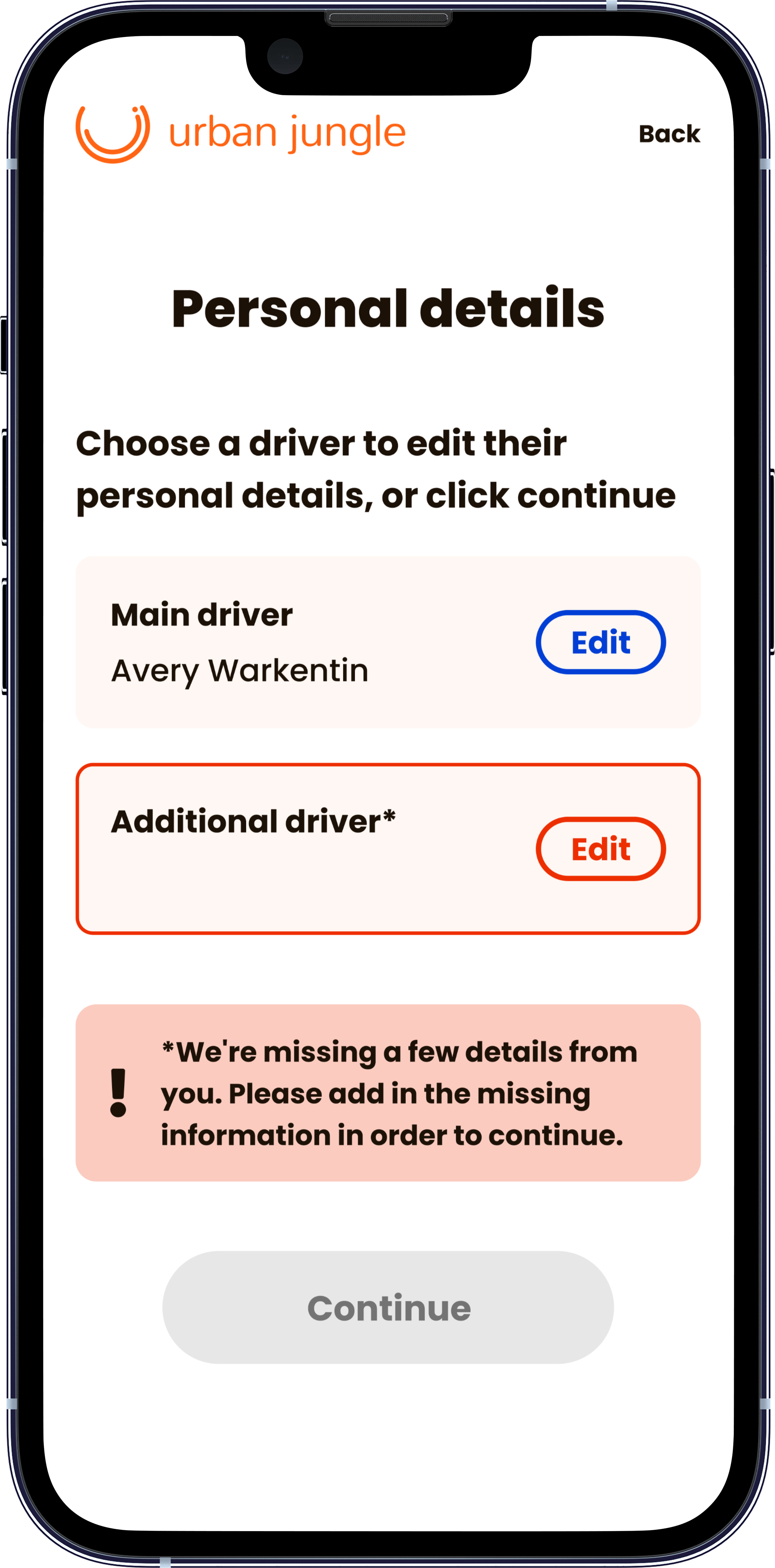

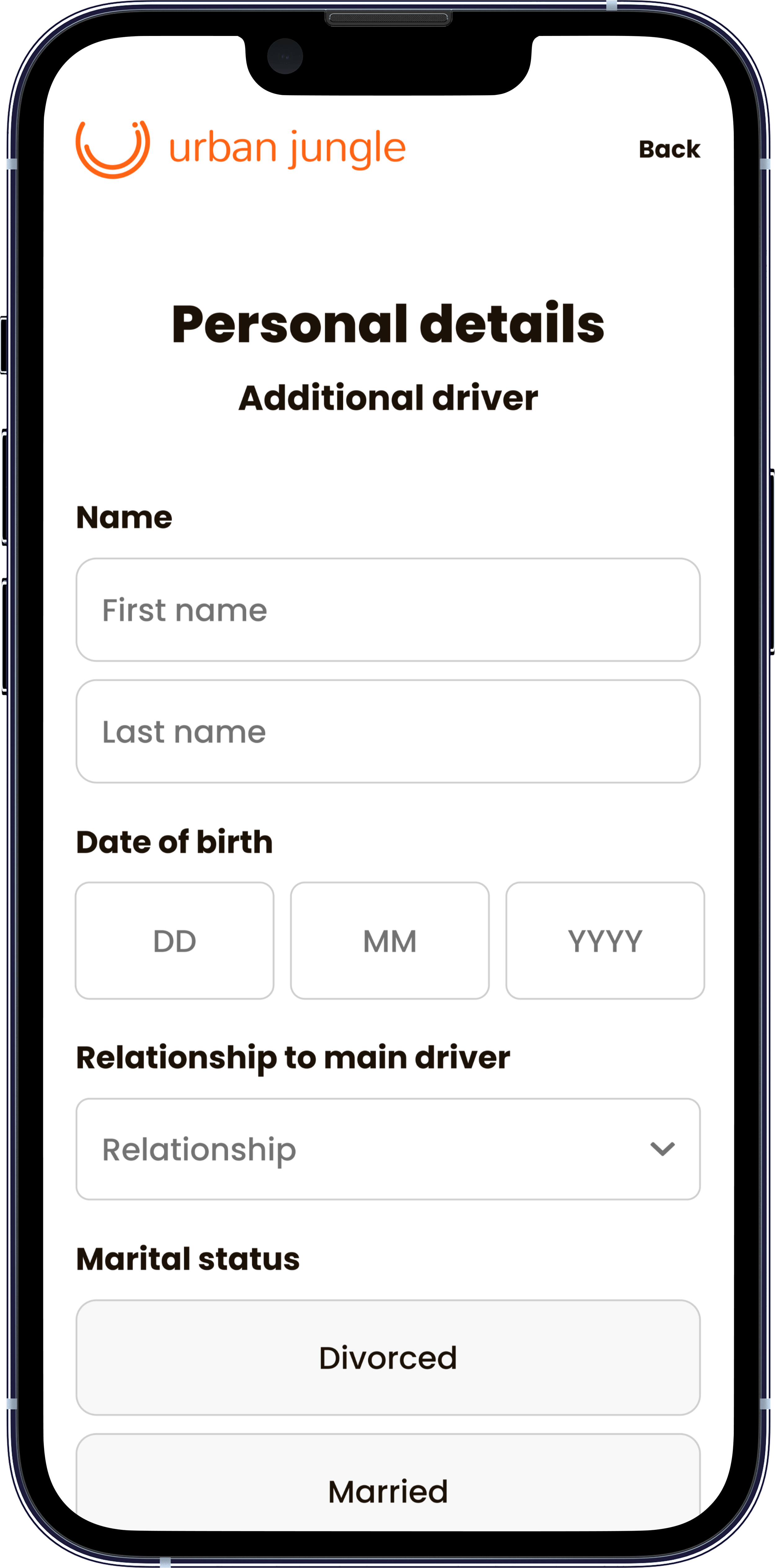

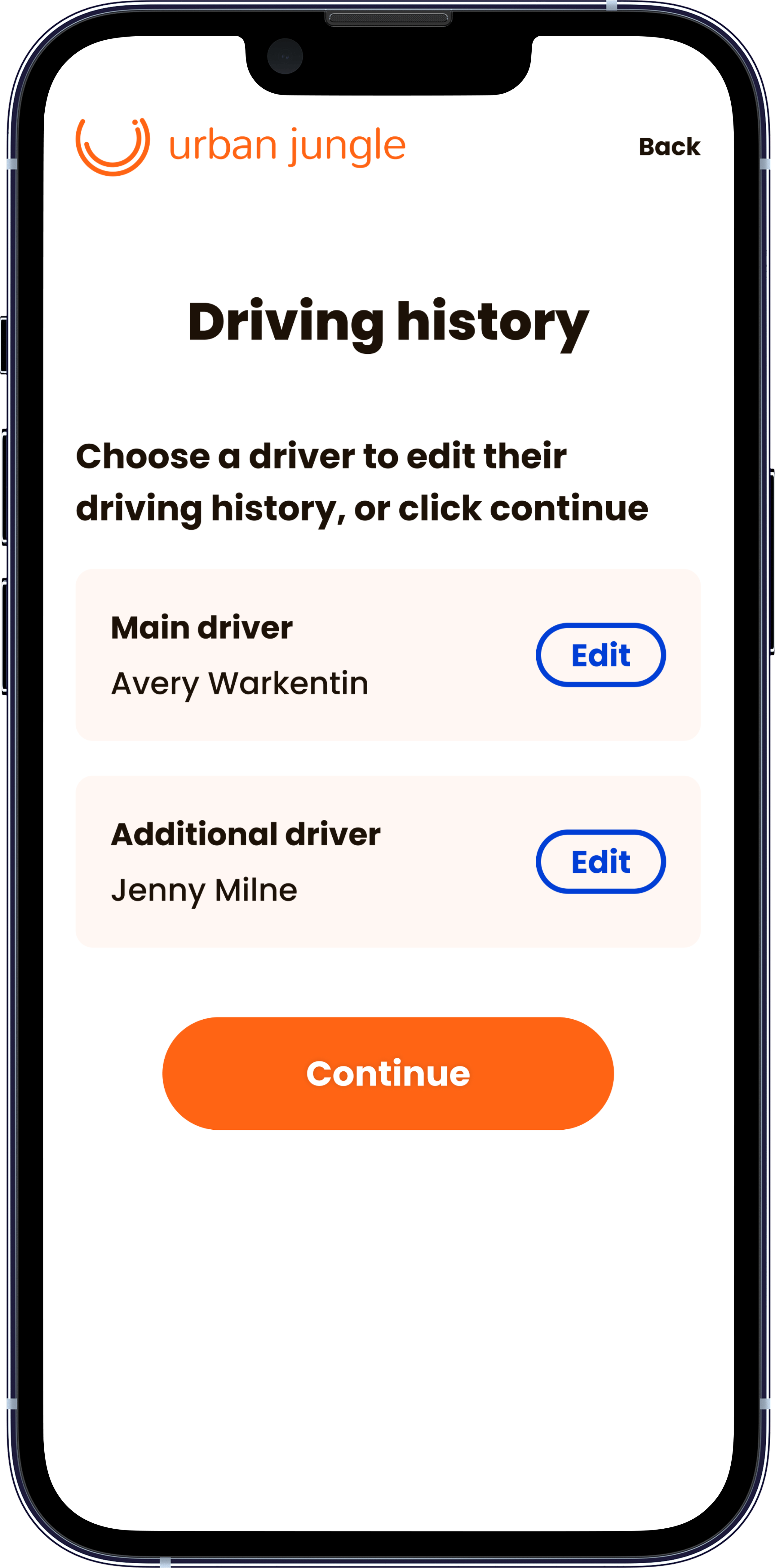

Additional Drivers — An Unexpected Challenge

The most iterated design challenge was the logic around adding additional drivers at purchase and MTA. Each additional driver requires information spread across multiple journey sections (Driver Details, Licence Details, and others) meaning a customer who adds a driver mid-journey has to navigate several separate sections before they can proceed.

We explored three approaches:

Collecting all additional driver questions upfront

Linking out to relevant sections

Using error indicators to surface missing information.

None were clean, and the eventual solution was shaped by engineering constraints that required clear structural separation of driver details.

We added a 'select driver' page within each section so customers could edit information per driver, with error messages tied to individual drivers rather than sections as a whole – making it immediately clear what was missing and for whom. Not the solution we'd have chosen at the beginning of the project, but the right one given the constraints.

Our solution: A ‘Select driver’ page to allow users to edit or add information per driver

Business Impact

Metric

Kick-off to launch

Post-launch phase

Average month-on-month growth

Conversion rate

Premium finance customers

Breakdown cover uptake

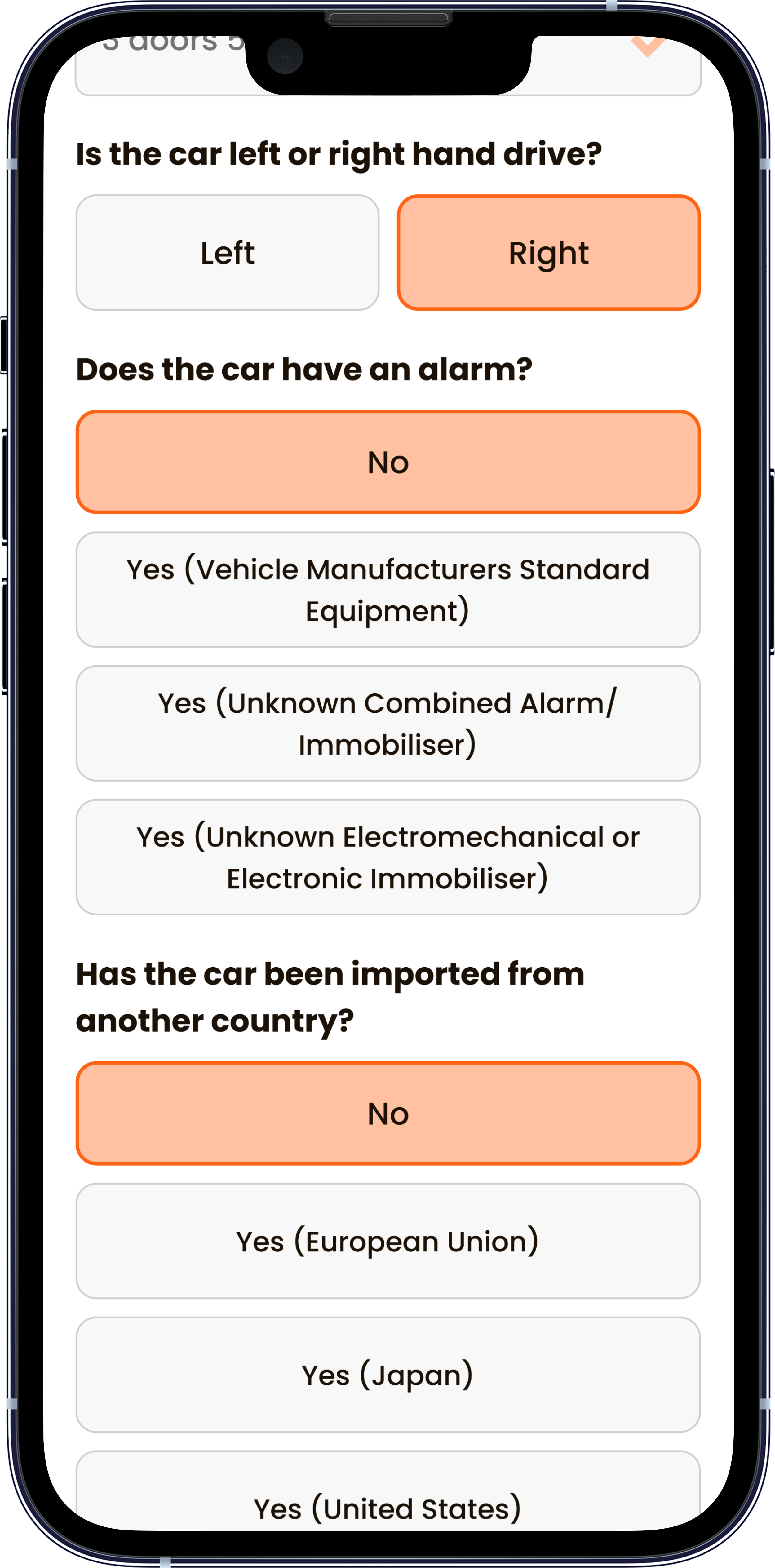

License and alarm types required mapping from our PCWs to OGI’s categories

Breakdown cover tier upsell rate

Breakdown cover tiers & Motor Legal expenses cover

Result

8 weeks

6 weeks

22% across first 9 months

Improving quarter-on-quarter

~40% of PCW purchasers

32%

24% of breakdown customers

Reflection

This project expanded how I think about third-party integrations and regulated product categories.

Understanding and designing around a premium finance provider (loan structures, repayment logic, deposit and arrears states) gave me a working knowledge of loan-based products that extends beyond just insurance. Premium finance customers represent a genuinely different subset of users with different financial circumstances and product needs, and designing for them required a different kind of empathy than the typical home insurance customer.

Car insurance also introduced a user motivation I hadn't encountered in home: legal obligation. Home insurance customers are choosing to protect something they value. Car insurance customers are required by law to have it. That changes the dynamic significantly. The design challenge shifts from communicating value to reducing friction and building enough trust that a legally required transaction doesn't feel punitive. Understanding that distinction changed how I approached information hierarchy, tone, and the overall rhythm of the journey.